Debt collection management in the US

Improve your company’s cash flow through efficient and compliant Debt collection management in the US solutions designed for financial managers of medium-sized enterprises.

¿What is Debt collection management in the US?

Debt collection management in the US refers to the set of strategies, tools, and legal processes that businesses use to recover unpaid invoices or overdue accounts. It encompasses both internal efforts and outsourced services provided by third-party collection agencies. This system ensures that companies can maintain healthy cash flows while complying with regulations such as the Fair Debt Collection Practices Act (FDCPA).

Effective debt collection management helps businesses avoid unnecessary losses and strengthen operational control. For financial managers, it’s essential to choose solutions that combine automation, data-driven insights, and legal compliance. With the support of Fig-Out, companies can implement systems that not only recover outstanding debts but also preserve customer relationships and protect the company’s reputation.

What laws regulate debt collection management in the United States?

In the U.S., debt collection activities are governed by several federal and state laws. The most important is the Fair Debt Collection Practices Act (FDCPA), which regulates third-party debt collectors and outlines their responsibilities when contacting consumers. Additionally, state-level regulations may vary and impose additional restrictions or licensing requirements.

Understanding and complying with these laws is essential for avoiding legal consequences and maintaining a professional reputation. Fig-Out ensures that all collection processes align with federal and state laws, protecting both creditors and debtors. Their legal expertise and compliance monitoring help businesses minimize risk while maximizing recovery.

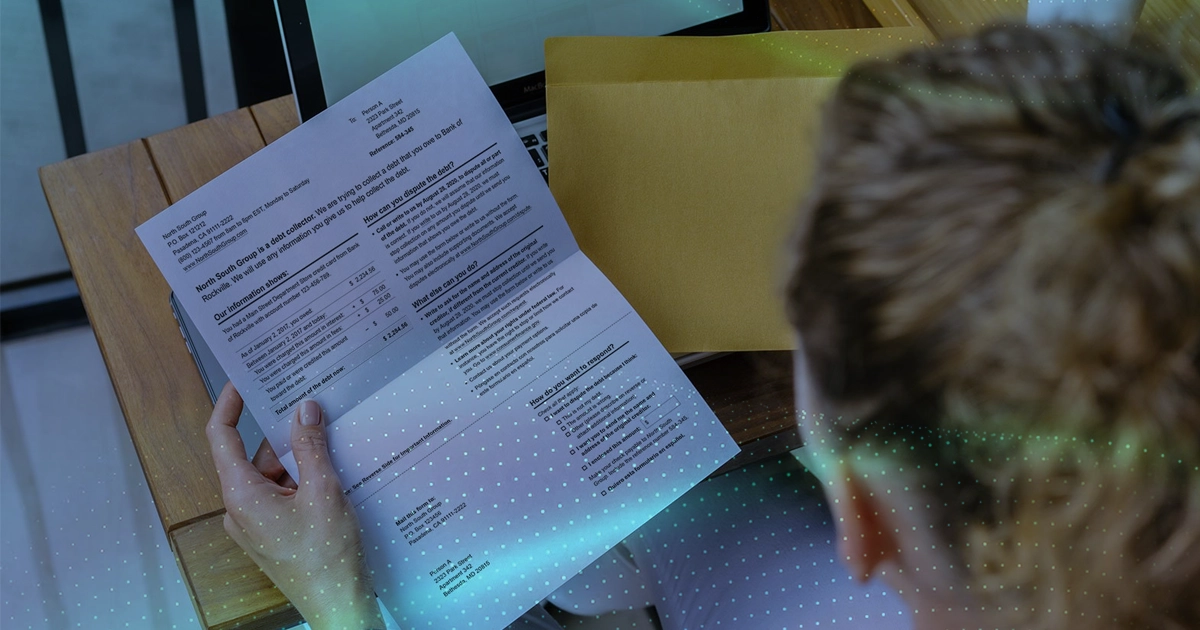

What is the Fair Debt Collection Practices Act (FDCPA) and how does it protect consumers?

The FDCPA is a federal law enacted in 1977 that protects consumers from abusive, deceptive, or unfair debt collection practices. It restricts when and how collectors may contact individuals and mandates that consumers receive written validation of the debt. Collectors must also identify themselves and their purpose during every communication.

For businesses, this means there are strict boundaries that must be respected. Partnering with Fig-Out guarantees that your collection efforts are executed ethically and in compliance with the FDCPA. This not only reduces the risk of lawsuits but also maintains the trust and dignity of your customer relationships.

What are the most effective methods to recover overdue debts in the U.S.?

Effective debt recovery involves a combination of early intervention, communication, and the use of digital tools. Automated reminders, call center follow-ups, and negotiated payment plans are among the most common and successful methods. When internal efforts fail, outsourcing to a professional agency is often the next best step.

Fig-Out combines advanced analytics with automation to track debtors’ behavior and recommend the best approach. Their team uses predictive models to prioritize high-probability collections and provides detailed performance reports. This data-driven strategy ensures that recovery is both efficient and client-friendly.

What is the difference between a debt collection agency and an internal collections department?

An internal collections department is managed by the company itself and handles early-stage delinquencies. Their focus is typically on maintaining customer relationships and recovering debts without involving legal procedures. In contrast, a debt collection agency specializes in recovering long-overdue accounts, often involving more persistent contact and legal action.

Choosing between internal and outsourced solutions depends on your company’s size, resources, and portfolio of delinquent accounts. Fig-Out offers hybrid solutions that integrate seamlessly with your internal systems and provide external expertise when necessary, ensuring optimal performance across all stages of the collection cycle.

What types of debts can legally be collected by third parties in the U.S.?

Third-party agencies in the U.S. can legally collect various types of consumer and commercial debts, including credit card debt, personal loans, medical bills, utility payments, and unpaid invoices. However, they must strictly follow legal protocols during every phase of the collection process.

With Fig-Out, businesses gain access to a team of trained professionals who specialize in multiple industries. Whether your company deals with B2B invoices or retail customers, Fig-Out ensures that collections are legally compliant and strategically customized for each case.

How does debt collection affect a person’s credit score in the U.S.?

When a debt is reported to credit bureaus as delinquent or charged off, it significantly impacts the individual’s credit score. Even settled debts may remain on credit reports for up to seven years, influencing their ability to get loans, credit cards, or housing.

Maintaining clear communication and offering repayment options can reduce the negative impact on a debtor’s score. Fig-Out promotes cooperative resolutions that help consumers repay in a manageable way while helping creditors recover funds without damaging long-term relationships.

What practices are prohibited for debt collection agencies in the U.S.?

Under the FDCPA, debt collectors are prohibited from using threats, harassment, or misleading statements. They cannot call at inconvenient hours, disclose debt information to third parties, or misrepresent the amount owed. Violations can lead to lawsuits and heavy fines.

Fig-Out adheres strictly to ethical and legal practices in all interactions. Their agents are trained in customer-centric communication techniques that promote understanding and cooperation. This approach increases recovery rates while protecting the company’s brand and avoiding litigation.

When is a debt considered uncollectible and what are the creditor’s options?

A debt is typically deemed uncollectible when the debtor has no assets, is unresponsive over time, or has declared bankruptcy. At this point, creditors can write off the debt as a loss, sell it to a collections firm, or pursue legal action if viable.

Fig-Out assists clients in assessing uncollectible accounts with precision. Their analytics tools help determine the probability of recovery, and their legal partners guide creditors through final resolution options such as debt sale or court action.

What are the steps to legally hire a debt collection agency in the U.S.?

Hiring a debt collection agency involves verifying their licensing, ensuring FDCPA compliance, and signing a service agreement that outlines terms, fees, and responsibilities. Agencies must also provide regular reporting and follow ethical guidelines during collections.

Fig-Out simplifies this process by offering vetted services and a transparent onboarding experience. Their team collaborates with your finance department to set goals, define KPIs, and maintain compliance throughout the engagement.

What actions can a consumer take if they believe they are being harassed by a collection agency?

Consumers who feel harassed can report the agency to the Consumer Financial Protection Bureau (CFPB), the Federal Trade Commission (FTC), or their state attorney general. They may also file lawsuits against abusive collectors and request that communication be limited or ceased.

Businesses can avoid being associated with such issues by partnering with ethical providers like Fig-Out. Their team respects consumer rights and emphasizes professional, respectful interactions that reflect positively on your brand and minimize reputational risks.